I get it. You are young and a long way from retirement, but in the greater scheme of things this is probably your most important benefit. At the end of your working career, the single largest asset you have should be your retirement savings.

Unlike health plans, retirement plans don’t vary that much from employer to employer. This is because the IRS and Employee Retirement Income Security Act rules dictate the basics of what most plans must contain and how they need to work. Most employers offer an IRS section 401k or 403b (for non-profit employers) qualified retirement plan. Here’s a look at the few variables that may differ from employer to employer.

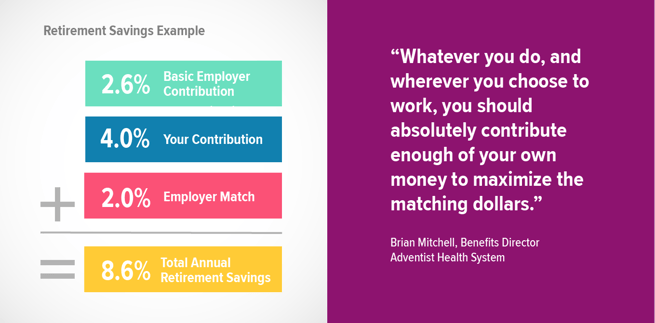

The Basic Employer Contribution

Many employers will make some type of contribution to your retirement plan even if you don’t. You may have to meet some eligibility criteria like working a certain number of hours during the year, but that is usually very achievable, especially if you have been employed for most of the plan year. This contribution is typically a percentage of your eligible earnings for the year. AdventHealth will make a basic contribution that is equivalent to 2.6% of your wages, up to the maximum wage limit allowed by the IRS.

The Employer Matching Contribution

This is an additional contribution that the employer will make as an incentive for you to contribute your own money to the plan. This is usually described as a certain amount for each dollar you contribute up to a certain level. AH will match 50% of the first 4% of wages that you contribute. Stated another way, for every 4% of your wages you contribute, AH will provide an additional 2% match so you end up with the equivalent of a 6% total contribution to your retirement account. Whatever you do, and wherever you choose to work, you should absolutely contribute enough of your own money to maximize the matching dollars.

Two Types of Vesting

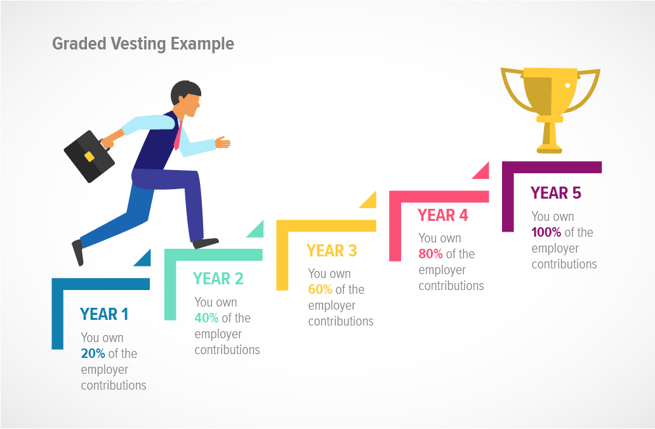

This is the amount of the employer contributions that you actually own. Because employers want you to stay with the company, they incorporate a vesting schedule that requires you to work for several years before you are vested (before you own) the contributions they have made to your account. If you quit before reaching 100% vesting you forfeit the unvested dollars. Most employers use one of two common vesting schedules.

Graded vesting means you own a fixed percent of the employer contributions for each year of employment. A standard graded schedule is one in which you own 20% of the employer contributions for each year of employment. After the first year you would own 20%, after two years you would own 40% and so forth, until by the end of year five you are 100% vested in the employer contributed dollars.

Cliff vesting is another common schedule. Under this approach you don’t own any of the employer dollars until you complete the required duration of employment, at which point you own 100% of the employer contributed dollars. AH uses a three-year cliff vesting schedule which means at the end of your third year you own all of the employer contributed dollars.

Automated Features

Many employers have incorporated automatic features that are designed to let inertia work to the advantage of the employee. We all get busy and sometimes forget to take care of important matters, so instead of having nothing happen until the employee makes decisions, these plan features will automatically enroll employees into the plan and may automatically increase your rate of contribution each year. They may also periodically rebalance your portfolio. These are all good things for you to do, and if they are done automatically then you don’t have to remember to do them yourself. It is like having your retirement savings on auto-pilot. But don’t worry, you can “opt-out” of these features if you want, but because they have such a positive impact on your retirement success you may want to reconsider any thoughts of “opting-out”.

Investing Options

Most plans provide you with 15-20 different investment fund options. Investment funds, such as mutual funds, are simply “baskets” of stocks and/or bonds that you purchase as an investment with your retirement savings contributions. There could be 100, 500, or even 2,000 stocks that have been pre-selected to be in a single mutual fund. Buying a “share” of a mutual fund helps you diversify and lower your investment risk by owning a little bit of many different companies instead of having all your money invested in just one or two companies.

Unless you are really into investing and have a lot of knowledge in that area, look for the target-date funds that should be available. These funds are set up to provide the right balance of stocks and bonds that are appropriate for your current age and expected retirement date. As you age, these funds are rebalanced to reflect an appropriate level of risk given the amount of time you have remaining until retirement. This is another great automatic feature that lets you “set it and forget it.” Keep in mind that although the value of investments in stocks and bonds can go up or down at any given time, the historical long-term trend has been up, which can provide a greater return on your money than lower interest savings accounts.

How Much to Save

So now that you know the basics, you are left with the primary question that most people have about retirement saving: How much do I need to save? You can calculate the exact amount if you know a few critical variables, like when you plan to retire, how much your annual living expenses will be at that time, and how long you’re going to live. Clearly these are variables that are very difficult to determine, so what are you supposed to do? It really isn’t as complicated as it might seem.

Four Steps to Maximize Your Retirement Savings

Here are four simple suggestions to help you successfully save for retirement.

1. Make sure you are enrolled (if not automatically enrolled) in the retirement plan and are contributing at least the percent that maximizes the employer’s matching contribution.

2. If possible, increase your contribution to 10% as quickly as you can. Remember, this contribution is deducted from your paycheck before you get your take home pay, so once you get accustomed to it you won’t miss it.

3. Unless you want to become an expert on investing, invest the dollars in the target-date fund associated with your anticipated retirement date.

4. Leave it alone. Most plans will have features like loans and hardship withdrawals that allow employees to take out funds for non-retirement related needs. Don’t do it. Forget these options are available. This is a retirement savings account and the funds contributed should be only for that purpose. If you need to fund your emergency savings or pay off high interest debt, then temporarily lower your retirement contribution (but not below the match level) for a few months and then quickly restore your retirement contributions back to their previous level.

In summary, the best thing you can do is start saving now, and let your steady contributions and time work to your advantage. As you watch your quarterly statements you will be surprised how quickly your account can grow.

Next Week: Time Off Benefits

Time off benefits are the most frequently used and one of the most misunderstood. Check out next week's post to learn more about how paid time off works and what kind of PDO we offer at AdventHealth. You can also learn more about how to compare employer benefits packages and medical benefits in these previous posts.